Every week we release educational videos related to hot topics in the mortgage industry on YouTube.

Subscribe to our channel to stay in-the-know!

Are you curious about how conventional conforming loans work and how they might apply to you? Each year, the Federal Housing Finance Agency (FHFA) reevaluates loan limits across the United States based on housing market trends. For 2025, these loan limits have increased again, making it easier for buyers to access affordable financing options with low down payments.

This post dives deep into the latest updates, the benefits and drawbacks of conventional loans, and tips for maximizing your mortgage potential.

You may hear the term Conventional Loan, or Conforming Loan or Conventional Conforming Loan. They are all the same. A conventional loan is a mortgage not backed by a government agency like FHA or VA loans. The term "conforming" refers to loans that adhere to the lending standards set by Fannie Mae and Freddie Mac, including loan size limits.

For 2025, the baseline conforming loan limit is $806,500, up from $762,000 in 2024. For high-cost areas, the maximum is $1,209,000, making homeownership more accessible in regions with soaring property values.

The formula for determining loan limits is based on the Housing Price Index (HPI) calculated by the FHFA. Here's how it works:

In high-cost areas (think California, New York, and parts of Virginia), limits are adjusted to reflect regional property values. Areas like Hawaii, Alaska, and Key West, Florida, also fall into the high-cost category.

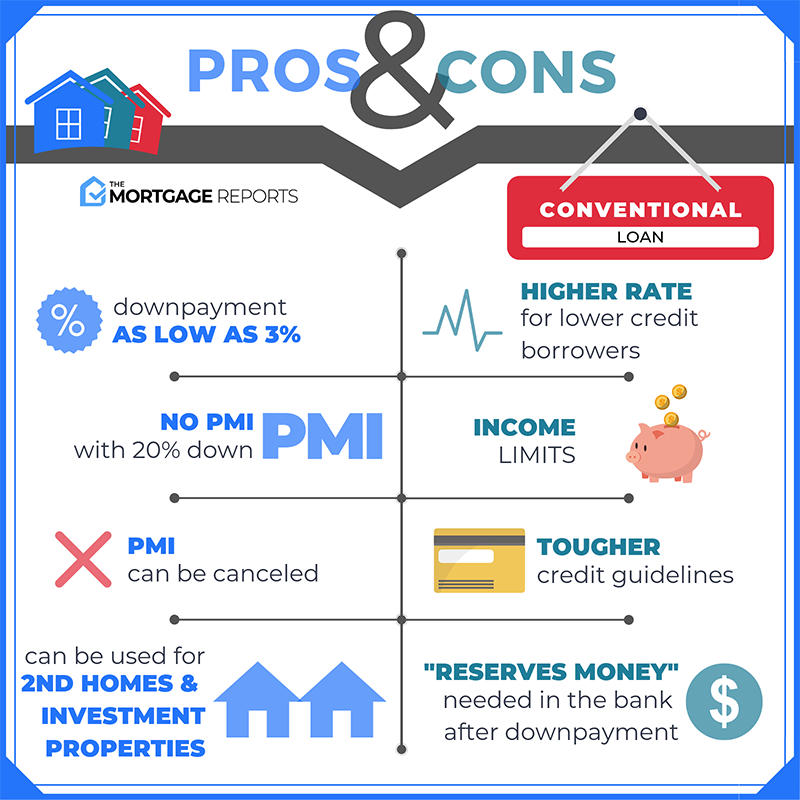

These loans come with several "superpowers" that make them a popular choice among buyers:

Conventional loans allow non-occupant co-borrowers, like parents or relatives, to help you qualify for a loan. This is especially helpful if you’re a first-time buyer with limited income.

If you've been self-employed for more than five years, you may qualify with just one year of tax returns, simplifying the approval process.

If you're moving out of your current home and plan to rent it, conventional loans allow you to count that rental income to offset your mortgage payment.

With conventional loans, you can finance up to four-unit properties with just 5% down if you plan to occupy one of the units. This is a fantastic way to start building wealth through real estate.

While conventional loans offer plenty of advantages, there are some potential downsides:

Conventional loans remain popular for their versatility and competitive terms. Here are some key reasons they stand out:

To dive deeper into the details mentioned above, check out these resources:

Conventional conforming loans are a powerful tool for homebuyers, offering flexibility, competitive rates, and options tailored to your financial situation. Whether you're a first-time buyer or a seasoned homeowner, conventional loans are a great option!

Looking for expert advice? Reach out to discuss your options and get pre-approved today.

All Rights Reserved | Jennifer Hughes Hernandez | Senior Loan Officer | NMLS #514497

Full service residential lender with an experienced team offering expert service, reliable communications and on-time closings in the greater Houston area.

Every week we release educational videos related to hot topics in the mortgage industry on YouTube.

Subscribe to our channel to stay in-the-know!

Gardner Financial Services, Ltd., dba Legacy Mutual Mortgage, NMLS #278675, a subsidiary of Prosperity Bank. 18402 U.S. Highway 281 N, Ste. 258, San Antonio, TX 78259. AZ BK-2001467. Check registration and licensing at nmlsconsumeraccess.org. Legacy Mutual Mortgage is an Equal Housing Lender. This is not a commitment to lend. Material is informational only and should not be construed as investment or mortgage advice. Legacy Mutual Mortgage is not an agency of the federal government. Not all loan products are available in all states. All loans are subject to credit and property approval. Not all applicants qualify. Restriction and conditions may apply. Information and programs current as of date of distribution but may change without notice. [11/2025]